Based on: Stefano DellaVigna, Matthew Gentzkow, Uniform Pricing in U.S. Retail Chains, The Quarterly Journal of Economics, Volume 134, Issue 4, November 2019, Pages 2011–2084, https://doi.org/10.1093/qje/qjz019.

The short version: Most major food, drugstore, and mass-merchandise chains in the U.S., charge essentially the same price in every store they operate, whether that store sits in a wealthy suburb or a lower-income neighborhood. According to a 2019 study in the Quarterly Journal of Economics, this costs the average chain roughly $16 million in forgone profit every year. Why they do it anyway remains, perhaps surprisingly, an open question.

The research, in slides (swipe or click through)

The setting

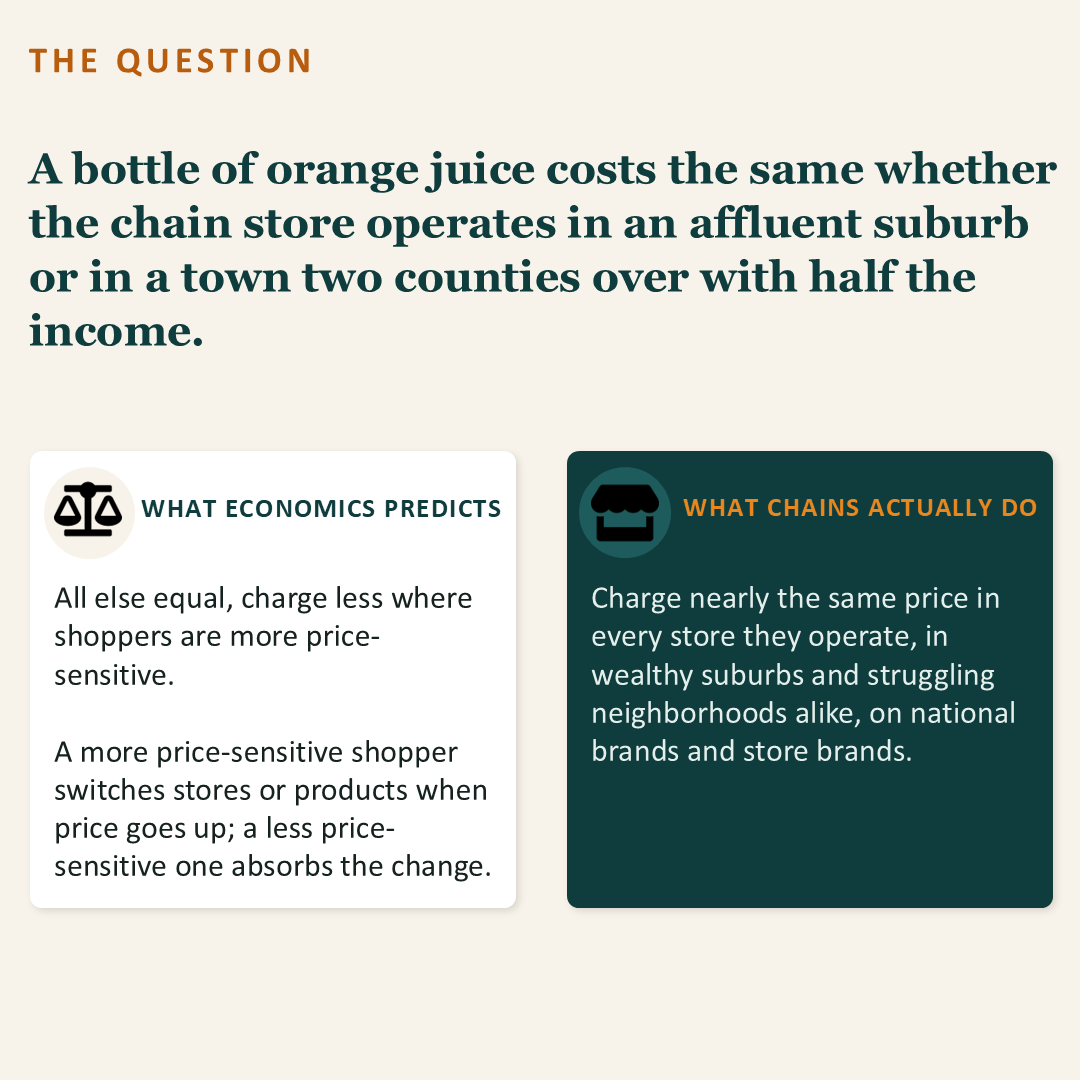

Walk into almost any major U.S. grocery chain and you will find that prices for national brands are essentially identical across every store in that chain, whether the store sits in a high-income suburb or a lower-income urban neighborhood. According to a 2019 study in the Quarterly Journal of Economics, this pricing uniformity costs the average chain millions of dollars in foregone profit every single year.

What economics predicts

The standard logic of pricing is straightforward. All else equal, a given price increase represents a bigger hit to a lower-income household’s budget than to a higher-income one, so lower-income shoppers tend to respond more sharply: switching products, skipping purchases, or traveling to a cheaper store. Higher-income shoppers, for whom the same price increase is a smaller share of their spending, tend to absorb it with less pushback. A profit-maximizing firm should price accordingly: lower where demand is more price sensitive, higher where it is less.

The method, plain English

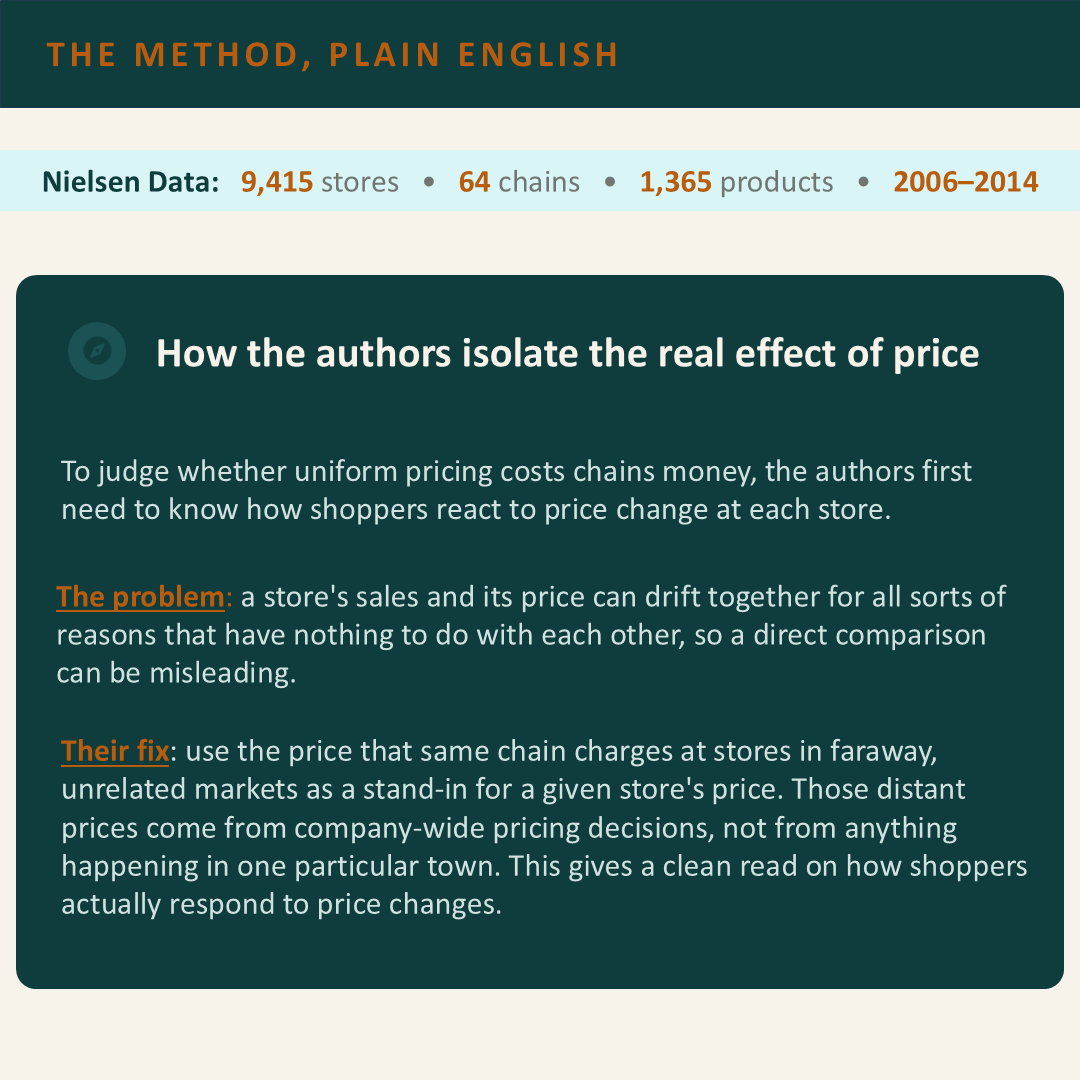

Stefano DellaVigna and Matthew Gentzkow analyzed Nielsen scanner data covering more than nine thousand food stores across sixty-four chains, tracking prices on 1,365 products, everything from soda to yogurt, over a nine-year period from 2006 to 2014.

To measure how uniform the pricing actually is, the researchers compared prices between pairs of stores within the same chain and pairs of stores in different chains across three dimensions: the average price difference over three-month periods, the week-to-week correlation in prices, and the share of weeks in which two stores charged prices within one percent of each other. Why three measures? Because they capture different dimensions of similarity that don’t always move together. Two stores could have highly correlated weekly prices due to same sale timing but very different regular prices, giving high correlation but high quarterly difference. Or similar average prices but different sale timing, giving low difference but low correlation. Using all three gives a more complete picture.

To assess whether uniform pricing was costing chains money, the researchers had to measure how shoppers react to price change. This is usually hard because prices often change right when demand is shifting, like raising chocolate or wine prices before Valentine’s Day, so it becomes hard to parse out the part of demand that responded to the price change and the part that changed simply because of the Valentine’s Day effect.

However, because these chains set prices uniformly, the authors can use price movements in a chain’s other stores as an instrument to help isolate how local shoppers respond to price changes. A pricing decision made at a distant headquarters is driven by national factors, like a broad promotional calendar, inventory levels, and chain-wide competitive pressures, none of which have anything to do with conditions in any single neighborhood. By looking at how a chain’s own stores in other parts of the country moved their prices, the authors could predict what any given store would charge in a particular week and use that prediction to isolate how shoppers responded to the price change, separate from anything else going on in their local neighborhood.

What the data show

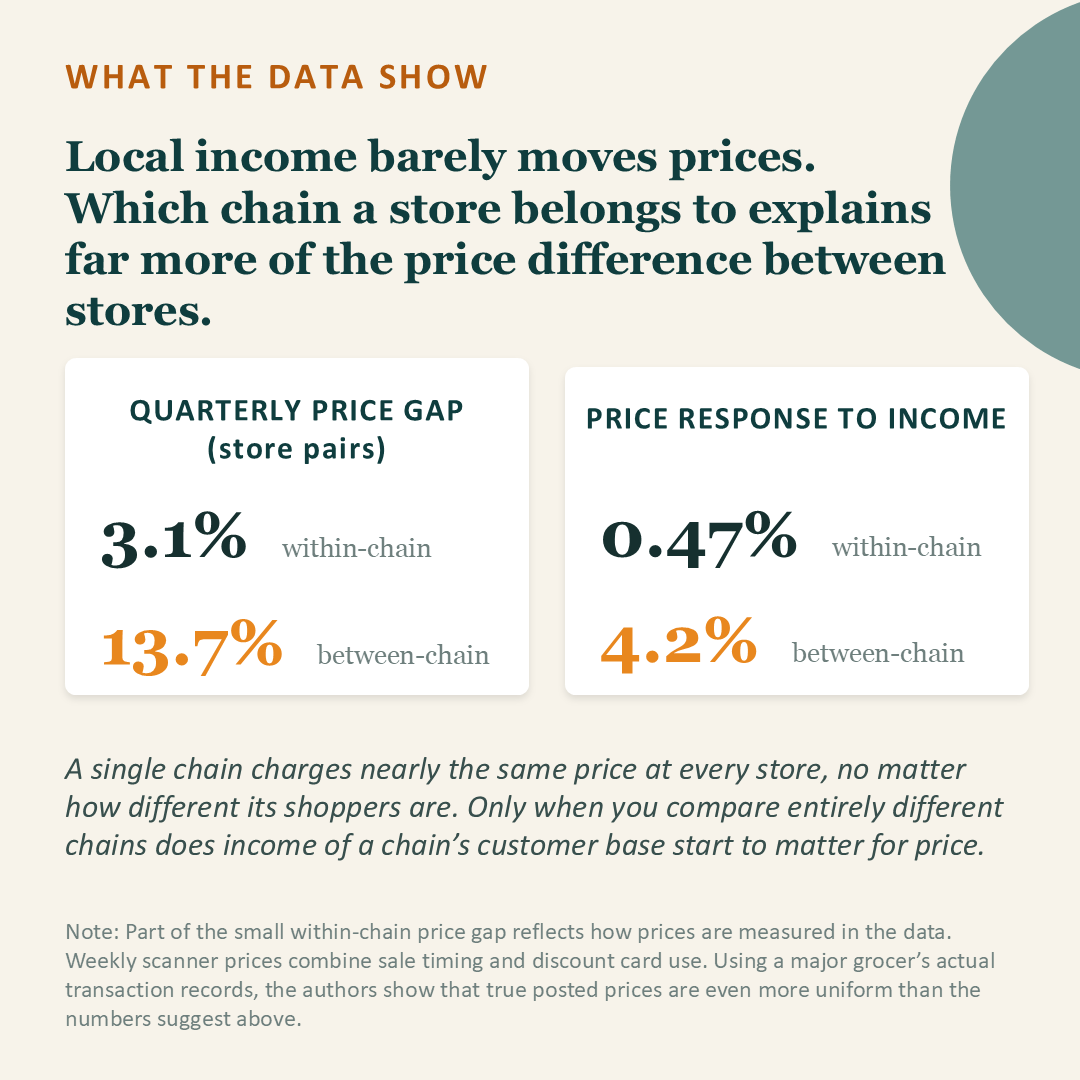

The evidence for uniform pricing is striking. Within a single chain, the average price difference between any two stores for the same product is only about 3%. Between different chains, that difference is four times larger. Even when comparing two stores of the same chain located in neighborhoods at opposite ends of the income spectrum, prices remain nearly identical. Ultimately, the chain brand name on the front of the store tells you far more about the price of orange juice in that store than the neighborhood it sits in.

The relationship between local income and local prices tells the same story. Within a chain, a store’s prices rise by only about 0.47% for every $10,000 increase in neighborhood income. In contrast, the price difference between different chains is nine times larger. While higher-price chains tend to serve higher-income customers on average, individual stores within those chains barely adjust their prices to reflect the income level of their local customer base.

The uniformity extends beyond prices to product assortment. The mix of products carried within a chain varies far less across stores serving different income levels than it does across different chains. Whether a store’s customers are predominantly higher-income or lower-income, they will likely find similar brands and items on the shelves if they are shopping at the same chain.

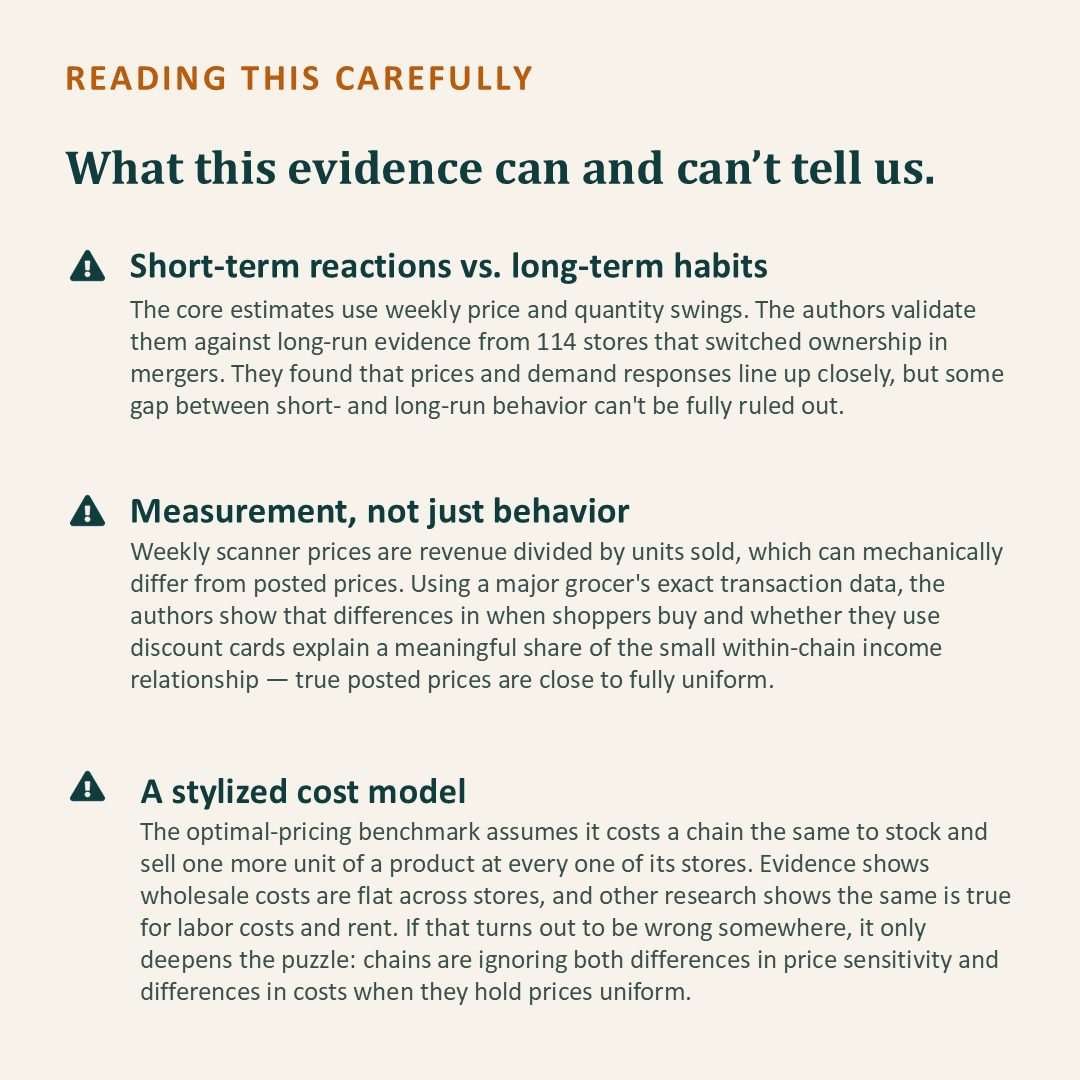

There’s a hidden layer of price uniformity in the data the researchers analyzed. The Nielsen data tracks the average price paid by all customers in a week, not the price on the shelf. The researchers discovered that some of the tiny within-chain price differences they did observe were a measurement quirk. Because shoppers in lower-income areas are more price-sensitive, they buy a larger share of their purchases during sale periods. This mechanically pulls down the average price paid in those stores, even when the shelf price is identical to every other store in the chain. Once the researchers corrected for this, prices looked even more uniform than the raw data suggested.

The findings

Using their demand estimates, the authors compute what prices each store should charge if the chain were maximizing profits. The gap between actual prices and what the model predicts is striking. Stores serving the least price-sensitive customers within a typical chain should charge about 17% more than stores serving the most price-sensitive customers. In reality, the difference is only about 0.4%. Because price sensitivity is closely tied to the average income of the customers a store tends to serve, this finding reveals that chains are largely failing to act on the fact that stores drawing higher-income shoppers face far less price resistance than stores drawing lower-income ones. While chains have figured out how to set their overall prices to match the markets they serve, they do not meaningfully adjust prices to local conditions across their own individual stores. In fact, authors estimate that stores adjust their prices to local demand at roughly one-tenth the rate that the model predicts they should.

This choice comes with a substantial price tag. The researchers estimate that by charging uniform prices rather than adjusting by store, the median chain sacrifices roughly $16 million in annual profit, representing 1.6% of its total revenue. For chains with the largest profit losses from uniform pricing, that figure exceeds $90 million per year. These are not marginal rounding errors. They represent a persistent gap between what these firms are doing and what their own demand conditions would support.

The most striking evidence comes from corporate mergers. When stores change ownership from one chain to another, their prices quickly begin to track the pricing pattern of the acquiring chain. This provides strong evidence that chain-level pricing policies play a major role in determining store prices.

Limitations worth knowing

While the findings are striking, they rest on a few key assumptions. First, the profit estimates assume that the cost of producing and delivering one additional unit of any given product is roughly the same across all stores in a chain, whether that store is in Manhattan or rural Ohio. The authors find that wholesale costs, which account for majority of a store’s total expenses, vary relatively little across stores across locations. They acknowledge, however, that they cannot fully account for every local variation in rent or labor costs. Importantly, the authors argue that if these local costs did vary, they would likely be positively correlated with the income level of the store’s customer base, meaning any cost variation would strengthen rather than weaken the paper’s core finding.

There is also the question of timing. The study primarily measures short-term reactions: how shoppers respond to a one-week price change. A chain setting permanent store-level prices would care more about longer-run responses, since shoppers have more time to adjust their habits and find alternatives. The authors use the merger data to show that long-run reactions are closely correlated with short-run ones, but they acknowledge this remains an area where more research could strengthen the conclusions.

Finally, the study focused on 1,365 frequently sold products, items like Coca-Cola and Simply Orange juice, to ensure clean comparisons across stores and chains. These are common items but represent only a slice of a grocery store’s total business. And because the data ends in 2014, it predates the growth of grocery delivery and personalized pricing tools that may be giving chains new ways to experiment with pricing today, a point we return to below.

What this means

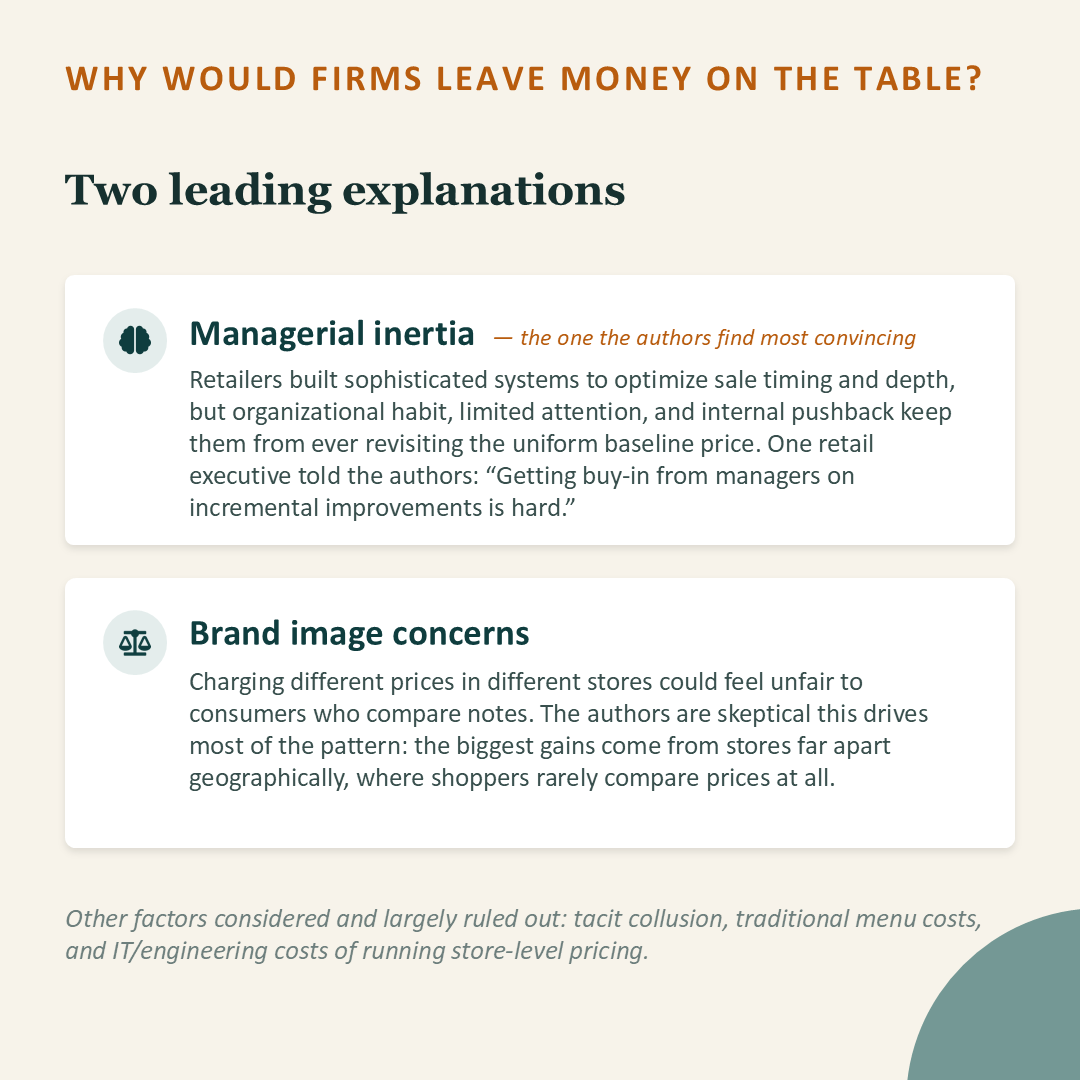

The authors suggest two main reasons why sophisticated chains leave so much money on the table. The first is managerial inertia: a mix of organizational barriers, limited attention, and internal politics. While retailers are experts at running complex national sales calendars, varying prices from store to store is a structural shift that most chains have simply not tackled. As one former executive told the authors, getting a team to change its pricing strategy is difficult when they are already focused on hitting existing budgets and margin targets. In the busy world of retail management, a missed opportunity is rarely the most urgent problem on anyone’s desk.

The second reason is brand image: the fear that customers will feel cheated if they discover different prices at different locations. The authors are skeptical that this is the primary driver. They note that few shoppers compare prices between cities, that optimal pricing would lower prices for lower-income customers rather than raise them, and that many other businesses, from fast-food chains to gas stations, already vary prices by location without visible backlash.

Four broader implications follow from the finding. First, uniform pricing likely worsens inequality in a specific and underappreciated way. Because flexible pricing would naturally lead to lower prices where customers are more price-sensitive, sticking to a single price means lower-income shoppers pay more than they would under optimal pricing. In a calibrated example, the authors estimate that shoppers in stores serving the lowest-income customers pay roughly 10% more relative to shoppers in stores serving the highest-income customers than they would under flexible pricing.

Second, uniform pricing weakens the response of prices to local economic conditions. Under flexible pricing, a local economic downturn would be expected to push retail prices downward as local demand weakens. Uniform pricing prevents this adjustment, leaving prices effectively stuck even when a locality is struggling.

Third, uniform pricing changes how we should think about retail mergers. Regulators typically analyze store competition market by market, asking whether two chains compete directly in the same neighborhood. But if a chain sets largely uniform prices across the country, a merger in one state can affect prices in markets where the merging firms do not even directly compete, because any price adjustment the merged entity makes will propagate across its entire store network simultaneously.

Fourth, uniform pricing affects how economists measure trade costs. Researchers often use price differences across locations to estimate the cost of shipping goods across the country. Uniform pricing compresses those price differences, making trade costs appear lower than they are and potentially distorting our understanding of how goods flow through the national economy

One dimension to keep in mind for readers in 2026

This paper predates the recent expansion of electronic shelf labels and AI-enabled retail technologies. Since its publication, several large retailers, including Walmart, have accelerated the rollout of electronic shelf labels to improve pricing accuracy and reduce the labor required to replace paper price tags. Walmart has also stated publicly that these labels are not intended to support surge pricing or individualized pricing. According to the company, prices remain the same for all customers shopping in a given store and are not determined by demand, the time of day, or the identity of the shopper.

At the same time, retailers have continued to expand loyalty programs that offer personalized digital coupons and promotions. These programs allow firms to tailor discounts to individual customers while leaving the posted shelf price unchanged. This distinction is important because the paper studies differences in posted store-level prices rather than individualized discounts or promotional offers.

The spread of electronic shelf labels has also prompted increased public and legislative scrutiny. Policymakers in several states and in Congress have proposed or passed legislation targeting surveillance pricing in grocery stores. Maryland became the first state to enact such a ban in 2026, and both the House and Senate have seen bills introduced aimed at restricting how retailers use consumer data to set prices. These proposals reflect concerns about how new pricing technologies could be used in the future rather than documented evidence that major grocery chains currently use electronic shelf labels to implement personalized shelf prices.

Taken together, these developments do not overturn the paper’s central finding. Large retailers continue to describe their pricing strategy as one based on uniform posted prices within a store, while increasingly using customer data to personalize promotions. Whether personalized discounts materially reduce the profit gap identified by DellaVigna and Gentzkow remains an open empirical question. The academic evidence has not yet established whether these newer technologies fundamentally change the economics of uniform pricing examined in this paper.

That naturally raises the next question. What happens when firms move beyond personalized promotions and begin using individual-level data to tailor prices directly?

In its next iteration, Economics Unpacked explores that question through the work of Jean-Pierre Dubé and Sanjog Misra. Rather than assuming that personalized pricing is either inherently harmful or inherently beneficial, they ask what happens to firms, consumers, and overall welfare when companies use individual-level information to set prices. Personalized pricing can increase firms’ profits, but its effects on consumer welfare depend critically on how consumers are segmented and how that information is used. Whether consumers are ultimately better or worse off turns out to be an empirical question rather than a foregone conclusion.